ASML stock review 2026: ASML holds a position that is unique in global technology. It is the only company on Earth that can build the machines needed to manufacture the most advanced semiconductors. Every cutting-edge chip inside your phone, your laptop, or the servers running AI models passed through an ASML machine. That kind of monopoly is rare, and it doesn’t come cheap. At a current price around €1,200 on Euronext Amsterdam, the stock trades at a premium that demands scrutiny. I dug into the numbers, the technology, and the risks.

Key Takeaways

- ASML is the sole manufacturer of EUV lithography systems, the machines required for chips below 7nm. No competitor exists.

- FY2025 revenue hit a record €32.7 billion with net income of €9.6 billion.

- Backlog stands at €38.8 billion as of Q4 2025, with 2026 guidance of €34 to €39 billion in revenue.

- SK Hynix placed a record $8 billion order on 24 March 2026, the largest single order in ASML’s history.

- The stock trades at roughly 49x trailing earnings, a premium, though below its late-2024 peak multiples.

- Key risks: China export restrictions, customer concentration, semiconductor cyclicality, and geopolitical exposure.

- Disclosure: I hold a long position in ASML, initiated March 2026.

Company at a Glance

| Detail | ASML |

|---|---|

| Sector | Semiconductor equipment |

| Headquarters | Veldhoven, Netherlands |

| Primary exchange | Euronext Amsterdam (ASML) |

| Secondary listing | NASDAQ (ASML) |

| ISIN | NL0010273215 |

| Employees | ~44,000 (2025) |

| FY2025 revenue | €32.7 billion |

| Market capitalisation | ~€470 billion (March 2026) |

| Index membership | AEX, EURO STOXX 50, STOXX Europe 600 |

| CEO | Christophe Fouquet (since April 2024) |

What Does ASML Do?

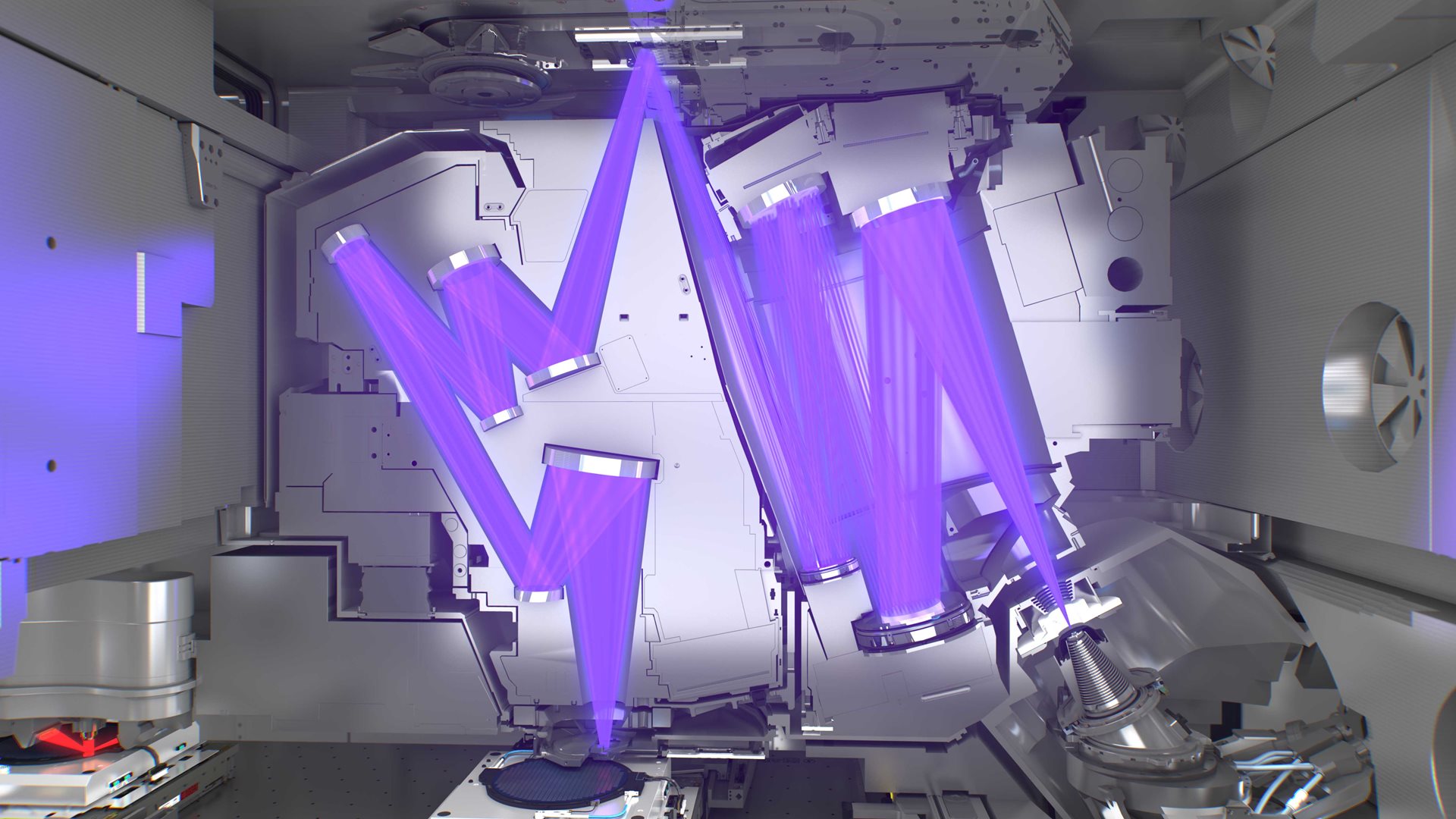

ASML makes lithography machines. That sounds dry until you understand what it means. Every semiconductor ever manufactured required a lithography step: projecting a circuit pattern onto a silicon wafer using light. For decades, the industry used deep ultraviolet (DUV) light at 193nm wavelength. That worked until physics said it couldn’t go smaller. To print the transistors needed for modern chips (billions of them, each smaller than a virus) the industry needed a completely different light source.

That light source is extreme ultraviolet (EUV), with a wavelength of just 13.5nm. Getting there took ASML and its partners over 30 years. The Veritasium documentary The Machine That Saved Moore’s Law captures the absurdity of the engineering involved: you fire a high-powered laser at tiny droplets of molten tin, 50,000 times per second, each droplet hit twice: once to flatten it, once to vaporise it into a plasma that emits EUV light. That light is then bounced off a series of mirrors so perfectly smooth that if you scaled one up to the size of Germany, the largest bump would be a millimetre tall.

Each EUV machine weighs about 180 tonnes, requires three Boeing 747s to ship, and costs upwards of €350 million. ASML recognised revenue on 48 EUV systems in 2025. Nobody else can build these machines. Intel tried to develop its own EUV capability decades ago and abandoned the effort. Nikon, once a competitor in DUV, never made the leap. ASML’s monopoly on EUV isn’t a moat. It’s an ocean.

But ASML isn’t only EUV. The company also dominates DUV lithography (used for less advanced but still critical chip nodes), and it sells metrology and inspection systems through its Computational Lithography division. In FY2025, EUV accounted for 48% of systems revenue (€11.6 billion, up 39% year-on-year) with DUV and other products making up the rest. The installed base of lithography systems worldwide also generates recurring service and upgrade revenue. Installed base management contributed €8.2 billion in FY2025, about 25% of total sales.

Financial Performance

ASML’s financials over the past five years tell a story of accelerating demand for advanced chipmaking equipment, punctuated by the usual semiconductor-cycle swings.

| Metric | FY2021 | FY2022 | FY2023 | FY2024 | FY2025 |

|---|---|---|---|---|---|

| Revenue (€B) | 18.6 | 21.2 | 27.6 | 28.3 | 32.7 |

| Net income (€B) | 5.9 | 5.6 | 7.8 | 7.6 | 9.6 |

| Net margin | 31.7% | 26.4% | 28.3% | 26.9% | 29.4% |

| Gross margin | 52.7% | 50.5% | 51.3% | 51.3% | 52.8% |

| EPS (€, basic) | 14.36 | 14.14 | 19.91 | 19.25 | 24.73 |

| Bookings (€B) | 26.2 | 30.7 | 20.0 | 18.9 | 28.0 |

A few things stand out. Revenue nearly doubled from 2021 to 2025, driven by surging demand for EUV machines. But bookings tell the more interesting story: they peaked at €30.7 billion in 2022, then fell to €20.0 billion in 2023 and €18.9 billion in 2024 as customers digested post-pandemic inventory. In October 2024, ASML accidentally leaked Q3 results showing weaker-than-expected orders. The stock dropped 16% in a single session. And then the cycle turned. Q4 2025 alone brought in €13.2 billion in new bookings, nearly double analyst expectations, and full-year 2025 bookings hit €28.0 billion. Semiconductor cycles haven’t been repealed, but AI demand is providing a powerful upswing.

Margins are striking. ASML consistently earns gross margins above 50% and net margins near 30%. For a hardware company shipping physical machines, those are software-like numbers. That’s monopoly pricing at work: when your customers have no alternative supplier, you set the terms.

The backlog at the end of Q4 2025 stood at €38.8 billion, providing strong visibility for the next 12 to 18 months. Management guided FY2026 revenue at €34 to €39 billion, implying continued growth at the midpoint.

Valuation

ASML’s valuation is the question that keeps potential investors up at night. Let’s look at the numbers without flinching.

| Metric | ASML | Applied Materials | KLA Corp | Lam Research |

|---|---|---|---|---|

| P/E (trailing) | ~49x | ~38x | ~40x | ~48x |

| P/E (forward) | ~34x | ~26x | ~32x | ~28x |

| EV/EBITDA (fwd) | ~35x | ~20x | ~32x | ~24x |

The entire semiconductor equipment sector trades at elevated multiples right now, inflated by AI capex expectations. ASML is the most expensive of the group, but the gap is smaller than you might expect. Lam Research trades at nearly the same trailing P/E (~48x), and KLA isn’t far behind (~40x). Applied Materials is the relative bargain at ~38x trailing.

So the question isn’t “why is ASML expensive?” but rather “does ASML deserve a premium even within an already expensive sector?” The argument for yes: ASML has a monopoly. The others don’t. Applied Materials, KLA, and Lam Research all compete with each other in etch, deposition, and inspection. ASML competes with nobody in EUV. That structural advantage, plus the recurring installed base revenue, earns it a higher multiple.

The argument for caution: at ~49x trailing earnings, the market is pricing in years of strong growth before ASML “grows into” this valuation. Historically, ASML’s P/E has ranged from the low 20s during down-cycles to the high 50s during peak euphoria. At current levels, it sits in the upper half of that range.

One way to think about it: if ASML hits the midpoint of its 2026 guidance (~€36.5 billion revenue) and maintains a 29% net margin, that’s roughly €10.6 billion in net income, or about €27 per share. At €1,200, that’s around 44x forward earnings. For a monopoly growing at mid-teens with decades of runway, some investors can stomach that. Others will wait for a pullback. Both positions are reasonable.

The Bull Case

AI capex is still accelerating

Every major AI model (GPT-5, Gemini, Llama) needs more compute, which means more advanced chips, which means more EUV machines. ASML’s own projections estimate the semiconductor market growing from around $600 billion in 2024 to over $1 trillion by 2030. The share of advanced nodes (where EUV is indispensable) keeps rising. SK Hynix confirmed this trajectory by placing a $8 billion order on 24 March 2026, the largest in ASML’s history, specifically for high-bandwidth memory (HBM) production, the chips that go into AI accelerators.

High-NA EUV is the next growth driver

ASML’s next generation machine, the Twinscan EXE:5000 (High-NA EUV), is now entering production at Intel and Samsung. These machines have a higher numerical aperture, enabling even finer chip patterns. They cost around $380 million (~€350 million) each, compared to roughly $200 million for the current generation. As leading chipmakers transition to 2nm and below, High-NA adoption should drive higher average selling prices and revenue growth well into the 2030s.

Installed base generates recurring revenue

With over 5,500 lithography systems in operation worldwide, ASML’s service and upgrade business generates predictable revenue that smooths out cyclical swings. In FY2025, installed base management contributed €8.2 billion in revenue (up 26% year-on-year). As the EUV installed base grows, this segment should compound. Customers can’t service these machines with third-party providers because the technology is too specialised.

Geopolitical reshoring benefits ASML

The global push to build domestic chip capacity (the CHIPS Act in the US, the European Chips Act, Japan’s semiconductor strategy) means more fabs being built in more places. Each new fab needs lithography equipment. The European Chips Act alone targets doubling EU chip production by 2030. More fabs, more ASML machines.

The Bear Case

China restrictions are a real revenue headwind

China was ASML’s second-largest market in FY2024, accounting for roughly 30% of systems revenue. US-led export controls, tightened in late 2024 and early 2025, now bar ASML from selling any EUV machines and some advanced DUV systems to Chinese customers. ASML has acknowledged that Chinese revenue will decline materially in 2026. The company managed the transition better than feared by reallocating capacity to other customers, but losing a third of your addressable market is not trivial.

Customer concentration is extreme

ASML’s three largest customers (TSMC, Samsung, and Intel) collectively account for the vast majority of EUV orders. If one of them delays capital expenditure (as Intel did in 2023), it ripples through ASML’s bookings. This concentration also gives these customers meaningful negotiating power. When TSMC asks for better terms, ASML has limited ability to say no.

Semiconductor cycles haven’t been abolished

The AI boom has made people forget that semiconductors are cyclical. The booking slump of 2023 and 2024 happened less than two years ago. If AI capex slows, whether because of a macro downturn, overbuilding, or slower-than-expected AI revenue for hyperscalers, ASML’s orders will feel it. The backlog provides a cushion, but it doesn’t make the company immune to cycles.

Valuation leaves little room for disappointment

At ~49x trailing earnings, the market is pricing in continued strong execution and growth. Any miss on guidance, margin compression from High-NA ramp costs, or geopolitical shock could trigger a meaningful de-rating. We saw this in October 2024 when ASML accidentally leaked Q3 results showing weaker bookings. The stock dropped 16% in a single day.

Dividend Profile

ASML is not a dividend stock, but it does return capital. The company proposed €7.50 per share in dividends for FY2025 (a 17% increase over FY2024’s €6.40), yielding roughly 0.6% at current prices. The payout ratio sits around 30% of net income, which is conservative and leaves room for growth.

More significant than the dividend is the buyback programme. ASML announced a new €12 billion share repurchase programme running through December 2028. Between dividends and buybacks, the company returns a substantial portion of its free cash flow. If you’re buying ASML for income, you’re buying the wrong stock. The thesis here is growth and capital appreciation, with the dividend as a modest bonus.

How to Buy ASML in Europe

ASML is one of the easiest European stocks to buy. It’s listed on Euronext Amsterdam under ticker ASML and on the NASDAQ under the same ticker. As a European investor, buying on Euronext avoids currency conversion fees entirely if you hold euros.

| Broker | ASML available? | Exchange | Approx. fee per trade (€5,000) |

|---|---|---|---|

| Interactive Brokers | Yes | Euronext AMS + NASDAQ | €1.25 to €3.00 |

| Degiro | Yes | Euronext AMS + NASDAQ | €2.00 (Euronext core selection) |

| Trade Republic | Yes | LSX (Lang & Schwarz) | €1.00 |

| Scalable Capital | Yes | gettex / Xetra | €0.99 to €3.99 |

If you plan to buy and hold, I’d lean towards Interactive Brokers or Degiro for direct Euronext access. Trade Republic and Scalable Capital route through alternative exchanges (LSX, gettex), which works fine for most retail orders but may have wider spreads during volatile sessions. For a full breakdown of costs and features, see our best brokers for European investors comparison. [AFFILIATE:IBKR] [AFFILIATE:DEGIRO]

My Take

I have a personal affinity for companies that build the foundational technology others depend on. In every gold rush, the most reliable profits go to whoever sells the shovels. ASML doesn’t just sell shovels for the AI gold rush. It is the only company that can make them.

What drew me to ASML wasn’t a financial ratio. It was understanding what EUV lithography involves: firing lasers at tin droplets in a vacuum, bouncing light off mirrors accurate to the width of an atom, all 50,000 times per second. The fact that this works at all, and that one company in the Netherlands figured out how to make it work reliably enough to ship dozens of machines a year, is one of the most remarkable engineering achievements in human history. When I find a company where the technology itself creates an unassailable competitive advantage, that catches my attention.

The risk is the price. At current multiples, you’re paying for excellence, and any stumble will hurt. I initiated a position in March 2026 because I believe the AI infrastructure buildout has years left to run and ASML sits at the very centre of it. But I’m not naive about cyclicality. I sized this position knowing that a 25 to 30% drawdown in a semiconductor downturn would not surprise me.

Disclosure: I hold a long position in ASML, initiated March 2026.

FAQ

Is ASML a good stock to buy in 2026?

ASML has strong fundamentals: monopoly position in EUV, growing backlog, and exposure to the AI capex cycle. However, the stock trades at a premium valuation that prices in continued growth. Whether it’s “good” depends on your time horizon and risk tolerance. This is not investment advice. Do your own research or consult a financial advisor.

Why is ASML the only company that makes EUV machines?

EUV lithography required over 30 years and billions in R&D to develop, involving breakthroughs in optics, laser technology, and precision engineering. ASML built this capability through deep partnerships with Carl Zeiss (optics) and Trumpf (laser source). The technical barriers are so high that no competitor, including Nikon, has been able to replicate the technology. Starting from scratch today would take decades and tens of billions of euros.

How do China export restrictions affect ASML?

US-led export controls prevent ASML from selling EUV systems and some advanced DUV systems to Chinese customers. China was roughly 30% of systems revenue in FY2024, so the impact is material. ASML has been reallocating capacity to customers in other regions, but the lost China revenue is a headwind for growth.

Can I buy ASML on Euronext in euros?

Yes. ASML’s primary listing is on Euronext Amsterdam (ticker: ASML). Most European brokers, including Interactive Brokers, Degiro, Trade Republic, and Scalable Capital, offer access. Buying on Euronext means you trade in euros and avoid currency conversion fees.

Does ASML pay a dividend?

Yes. ASML proposed €7.50 per share for FY2025, yielding approximately 0.6% at current prices. The dividend has grown consistently over the past decade, though the yield remains modest. ASML also returns capital through share buybacks.

Methodology

This stock review is based on ASML’s publicly filed annual reports and quarterly earnings releases, regulatory filings, third-party financial data from Yahoo Finance and Morningstar, and industry analysis from SEMI. The EUV technology explanation draws on the Veritasium documentary linked above. Valuation peer comparisons use trailing and forward estimates from consensus analyst data as of March 2026. All financial figures are in euros unless otherwise stated. I last verified these numbers on 25 March 2026.

Disclaimer: This article is for informational and educational purposes only. It is not investment advice. I may hold positions in the securities discussed, and in the case of ASML, I do hold a long position initiated in March 2026. Past performance does not guarantee future results. Investing involves risk, including the possible loss of principal. Always do your own research or consult a qualified financial advisor before making investment decisions.

Affiliate disclosure: Some links in this article are affiliate links. If you open an account through these links, The Bourse Report may receive a commission at no additional cost to you. This does not influence our editorial opinions. We recommend only brokers we’ve personally used and tested. See our editorial policy for details.

Keep Reading

- TotalEnergies at €79: A Dangerous Bet on Brent — Another European blue-chip under the microscope.

- Best Online Brokers for European Investors 2026 — Where to buy ASML and other European stocks.

- How to Buy US Stocks in Europe — ASML also trades on NASDAQ. Here is how to access it.

- How to Spot a Pump and Dump — Protect yourself from stock manipulation schemes.

Leave a Reply